Ch. 9: Net Present Value and Other Investment Criteria

Capital Budgeting

- What fixed assets should we buy? What projects should we invest in?

- Goal of Management: Maximize shareholder value

- How do we evaluate capital budgeting decision rules?

- Does the decision rule adjust for the timing of the cash flows? (TVM)

- Does the decision rule appropriately adjust for risk?

- Does the decision rule provide information on value creation?

- How does capital budgeting differ from valuing stocks and bonds?

- Unlike stocks, projects have cash flows that end.

- Project cash flows typically vary through time, unlike a fixed coupon or a dividend that grows at a constant rate.

Example

- You are reviewing a new project and have estimated the following cash flows:

- Year 0: CF = –165,000

- Year 1: CF = 63,120; NI = 13,620

- Year 2: CF = 70,800; NI = 3,300

- Year 3: CF = 91,080; NI = 29,100

- Average Book Value = 72,000

- Your required return for assets of this risk level is 12%.

Capital Budgeting Decision Rules

- Net Present Value (NPV)

- Does the PV of cash inflows exceed the PV of cash outflows?

- If the NPV is positive, accept the project.

- In the case of our example, NPV is $12,627.41.

- Use financial calculator’s CF registry.

- Do we accept or reject the project?

- Does this rule meet our criteria for a good capital budgeting decision rule?

- Does the decision rule adjust for the timing of the cash flows? Yes.

- Does the decision rule appropriately adjust for risk? Yes.

- Does the decision rule provide information on value creation? Yes.

- Payback Period

- How long does it take to get the initial cost back in a nominal sense?

- If the payback period is shorter than some preset limit (typically 3–4 years), accept the project.

- In the case of our example, payback occurs in 3 years (2.34 if cash flows are evenly spaced throughout the year).

- Consider a benchmark payback period of 3 years.

- Do we accept or reject the project?

- Does this rule meet our criteria for a good capital budgeting decision rule?

- Does the decision rule adjust for the timing of the cash flows? No.

- Does the decision rule appropriately adjust for risk? No.

- Does the decision rule provide information on value creation? No.

- Consider two projects. One project costs $250 and pays out $100 each year over the next 4 years. The other project costs $250, pays out $100 in year one, and pays out $200 in year two. Assume a required rate of return of 15 percent.

- Payback period: 2.5 years vs. 1.75 years

- NPV: $35.50 vs. $–11.81

- Features:

- Easy

- Biased toward liquidity (short-term projects)

- Accounts for the uncertainty of long-term cash flows by ignoring them entirely

- Discounted Payback Period

- How long does it take to get the initial cost back after discounting the cash flows?

- If the discount payback period is shorter than some preset limit, then accept.

- In the case of our example, payback occurs in 3 years.

- Consider a benchmark payback period of 2 years.

- Do we accept or reject the project?

- Does this rule meet our criteria for a good capital budgeting decision rule?

- Does the decision rule adjust for the timing of the cash flows? Yes.

- Does the decision rule appropriately adjust for risk? Yes.

- Does the decision rule provide information on value creation? No. The cutoff period is arbitrary.

- Average Accounting Return

- What is the ratio of average net income to average book value?

- If the average accounting return exceeds some threshold, accept the project.

- In the case of our example, AAR is 21%.

- Consider a benchmark AAR of 25%.

- Do we accept or reject the project?

- Does this rule meet our criteria for a good capital budgeting decision rule?

- Does the decision rule adjust for the timing of the cash flows? No.

- Does the decision rule appropriately adjust for risk? No.

- Does the decision rule provide information on value creation? No.

- This rule doesn’t even account for cash flows.

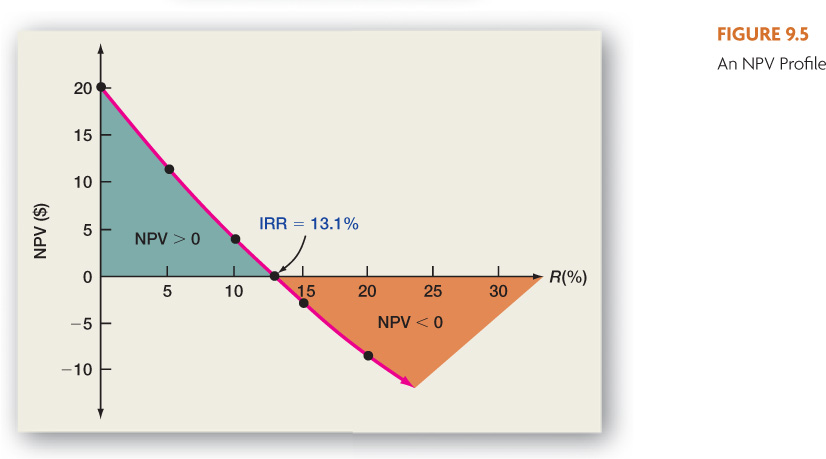

- Internal Rate of Return (IRR)

- What rate of return makes the NPV zero?

- If the IRR exceeds the required rate of return, then accept.

- In the case of our example, IRR is 16.13%.

- CF registry on financial calculator

- Trial and error, otherwise

- Remember relationship between price and rate of return.

- If NPV > 0, then increase the IRR.

- If NPV < 0, then decrease the IRR.

- Do we accept or reject the project?

- See Figure 9.5

- Does this rule meet our criteria for a good capital budgeting decision rule?

- Does the decision rule adjust for the timing of the cash flows? Yes.

- Does the decision rule appropriately adjust for risk? Yes.

- Does the decision rule provide information on value creation? Yes.

- Generally, NPV and IRR give the same decision, except:

- CFs that change sign more than once

- Consider a strip mine that costs $60. The cash flows are $155 in the first year and -$100 in the second year.

- The NPV is zero when the IRR is 25% and when the IRR is 33.33%.

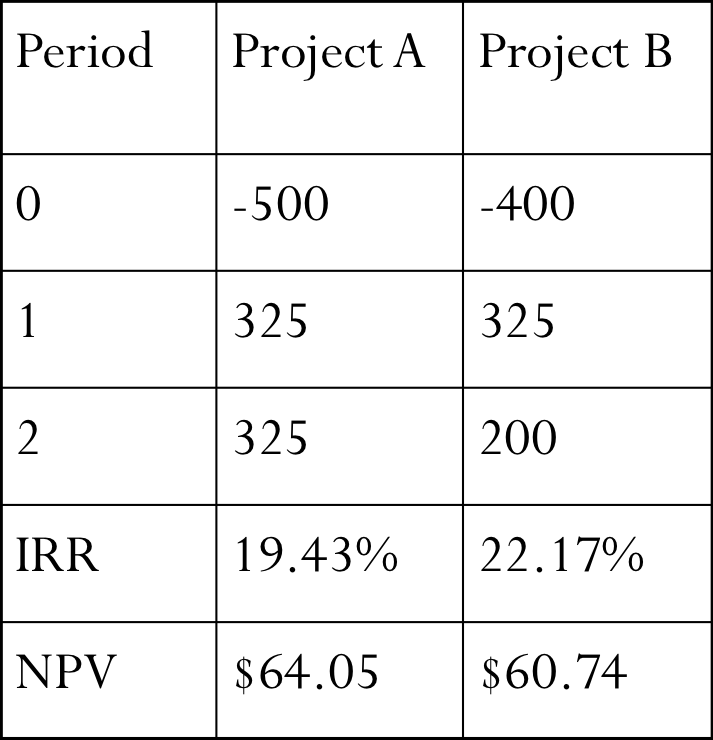

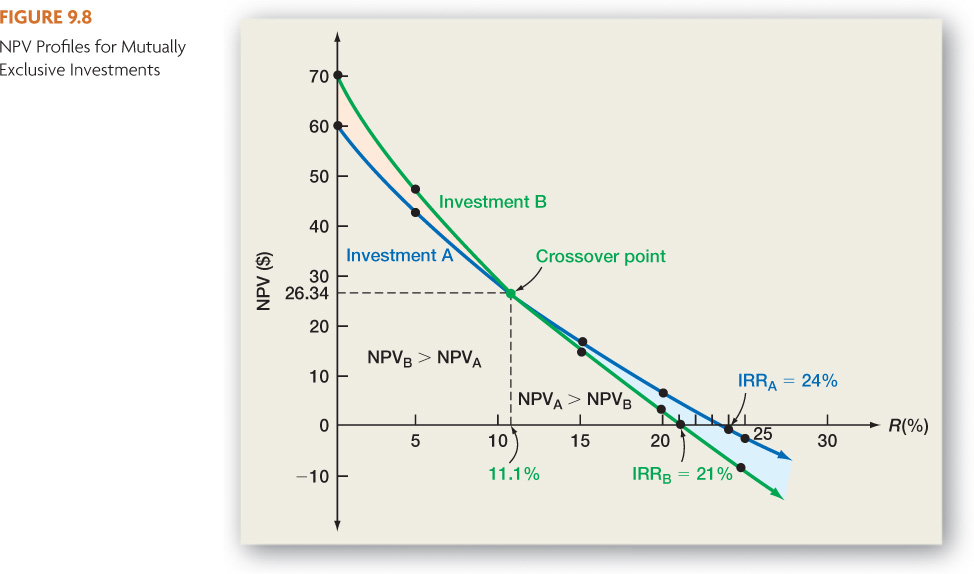

- Mutually exclusive investments

- A situation in which taking one investment prevents the taking of another.

- See Example

- See Figure 9.8

- Crossover Rate

- The discount rate that makes the NPVs of the two projects equal

- Example

- Investment A CFs: -$400, $250, $280

- Investment B CFs: -$500, $320, $340

- Work with NPV(B-A) to find crossover.

- In the case of conflicts, always use NPV.

- Modified IRR

- Return to our previous example

- Consider a strip mine that costs $60. The cash flows are $155 in the first year and -$100 in the second year.

- The NPV is zero when the IRR is 25% and when the IRR is 33.33%.

- The required rate of return is 20%.

- Method 1: Discounting Approach

- Discount negative cash flows to present at the required rate of return.

- Now the initial cash flow is -$129.44, and the MIRR is 19.74%.

- Method 2: Reinvestment Approach

- Reinvest cash flows at the required rate of return.

- Now the only inflow is $86 at year two, and the MIRR is 19.72%.

- Method 3: Combination Approach

- Discount negative cash flows to present.

- Compound positive cash flows to end.

- CF0 is -$129.44, CF2 is $186, and the MIRR is 19.87%.

- Profitability Index

- What is the ratio of the present value of cash flows to the cost of the project? (this is equal to 1 + NPV/Cost)

- If PI > 1, then accept.

- Can lead to ranking problems in mutually exclusive investments.

- Investment A: $5 cost, $10 PV of cash flows

- Investment B: $100 cost, $150 PV of cash flows

In Practice

- Multiple criteria are used (NPV/IRR primary, Payback Period secondary)

- Why?

- Liquidity may be an issue

- NPV calculations can be costly/time consuming

- Cash flows may be uncertain (``soft’’ NPV)

- Tie performance to firm value

Practice Problem

- An investment project has the following cash flows: CF0 = –1,000,000; C01 – C08 = 200,000 each

- If the required rate of return is 12%, what decision should be made using NPV?

- How would the IRR decision rule be used for this project, and what decision would be reached?

- How are the above two decisions related?

{kind=link}

{kind=link}

{kind=link}