Ch. 6: Discounted Cash Flow Valuation

Multiple Cash Flows

- Make an apples to apples comparison. Every cash flow must be in the same $-year.

- Suppose you have $\$$1,000 now in a savings account earning 6%. You want to add $\$$500 one year from now and $\$$700 two years from now.

- How much will you have in two years?

- How would we value the entire stream after year one?

- What about at year five?

Calculator Practice

- Your broker calls you and tells you that he has this great investment opportunity. If you invest $\$$100 today, you will receive $\$$40 in one year and $\$$75 in two years. If you require a 15% return on investments of this risk, should you take the investment?

Equal Cash Flows Case

- Perpetuity

- infinite series of equal payments

- $PV = C/r$

- Annuity

- finite series of equal payments that occur at regular intervals

- If the first payment occurs at the end of the period, it is called an ordinary annuity.

- If the first payment occurs at the beginning of the period, it is called an annuity due.

- $PV = C[\frac{1-\frac{1}{(1+r)^t}}{r}]$

- $FV = C[\frac{(1+r)^t–1}{r}]$

Practice

- After carefully going over your budget, you have determined you can afford to pay $632 per month towards a new sports car. You call up your local bank and find out that the going rate is 1 percent per month for 48 months. How much can you borrow?

- Suppose you win the Publishers Clearinghouse $\$$10 million sweepstakes. The money is paid in equal annual end-of-year installments of $\$$333,333.33 over 30 years. If the appropriate discount rate is 5%, how much is the sweepstakes actually worth today?

- You are ready to buy a house, and you have $\$$20,000 for a down payment and closing costs. Closing costs are estimated to be 4% of the loan value. You have an annual salary of $\$$36,000, and the bank is willing to allow your monthly mortgage payment to be equal to 28% of your monthly income. The interest rate on the loan is 6% per year with monthly compounding (.5% per month) for a 30-year fixed rate loan.

- How much money will the bank loan you?

- How much can you offer for the house?

Finding the Payment

- Suppose you want to borrow $20,000 for a new car. You can borrow at 8% per year, compounded monthly. If you take a 4-year loan, what is your monthly payment?

Finding the Number of Payments

- You ran a little short on your spring break vacation, so you put $\$$1,000 on your credit card. You can only afford to make the minimum payment of $\$$20 per month. The interest rate on the credit card is 1.5 percent per month. How long will you need to pay off the $\$$1,000?

Finding the Rate

- Trial and Error

- If PV > loan amount, then interest rate is too low.

- If PV < loan amount, then interest rate is too high.

- Suppose you borrow $\$$25,000 from your parents to buy a car. You agree to pay $\$$207.58 per month for 60 months. What is the monthly interest rate?

Annuity Due and Timing

- If you use the regular annuity formula, the FV will occur at the same time as the last payment.

- You are saving for a new house and you need 20% down to get a loan. You put $\$$10,000 per year in an account paying 8%. The first payment is made today. How much will you have at the end of 3 years (you make a total of three $\$$10,000 payments)?

What if Cash Flows Grow?

- Perpetuity: $PV = \frac{C}{r-g}$

- Annuity: $PV = C[\frac{1-(\frac{1+g}{1+r})^t}{r-g}]$

Effective Annual Rate vs. Annual Percentage Rates

- APR - the interest rate expressed in terms of the interest payment made each period

- EAR - the interest rate expressed as if it were compounded once per year

- Useful in comparing two securities with different compounding frequencies.

- You are looking at two savings accounts. One pays 5.25%, with daily compounding. The other pays 5.3% with semiannual compounding.

- Story of compounding

- $EAR = (1+\frac{APR}{m})^m - 1$ where $m$ is the number of compounding periods per year

- Alternatively, you can calculate PV to FV then back.

- What rate is a credit card likely to quote? What about a savings account?

- A payday lender allows you to write a check for $\$$115 dated 14 days in the future, for which you get $\$$100 today. What is the APR? EAR?

- Continuous compounding: $EAR = e^q–1$

Loan Types

- Pure discount loans - no periodic interest payments

- Interest-only loans - repay interest each year

- Amortized loan with fixed principal payment - pay interest plus fixed portion of principal. See

- Amortized loan with fixed payment - pay fixed payment. Fixed payment covers interest first with the remainder reducing principal.

- Partially amortized loan with balloon payment

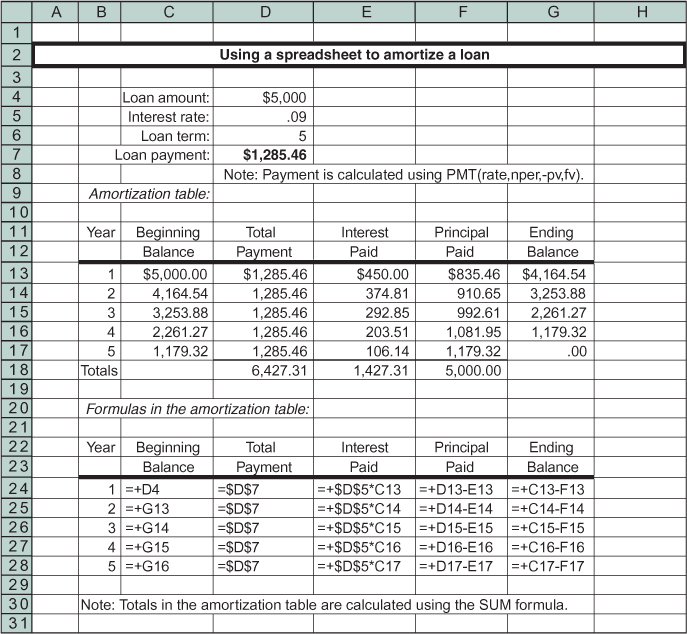

Example: Amortized loan with fixed payment

Example: Partial Amortization

- Suppose we have a $100,000 commercial mortgage with a 12% APR and a 20-year amortization schedule. What will the monthly payment be? What will the balloon payment after 5 years be?

{kind=link}