Ch. 2: Financial Statements, Taxes, and Cash Flow

Balance Sheet

- Snapshot of the firm

- Balance Sheet Identity: Assets = Liabilities + Equity

- Piece by piece

- Assets

- Current Assets

- < 1 year life

- inventory, cash, accounts receivable

- Fixed Assets

- Tangible: plants, property, and equipment

- Intangible: patents, trademarks, and intellectual property

- Liabilities

- Current liabilities

- Due in < 1 year

- Accounts payable

- Long-term debt (bonds)

- Equity (residual claim)

- Net Working Capital: Current Assets - Current Liabilities

- Evaluating a balance sheet

- Liquidity

- ease of conversion vs. loss of value

- protection against financial distress vs. forgone potential profits

- Leverage

- debt vs. equity

- serves to magnify gains and losses to equity

- Market value vs. book value

- Book value: historical cost (subject to GAAP)

- Market value: price the market will bear

- What drives the difference? (depreciated asset that still generates cash flows)

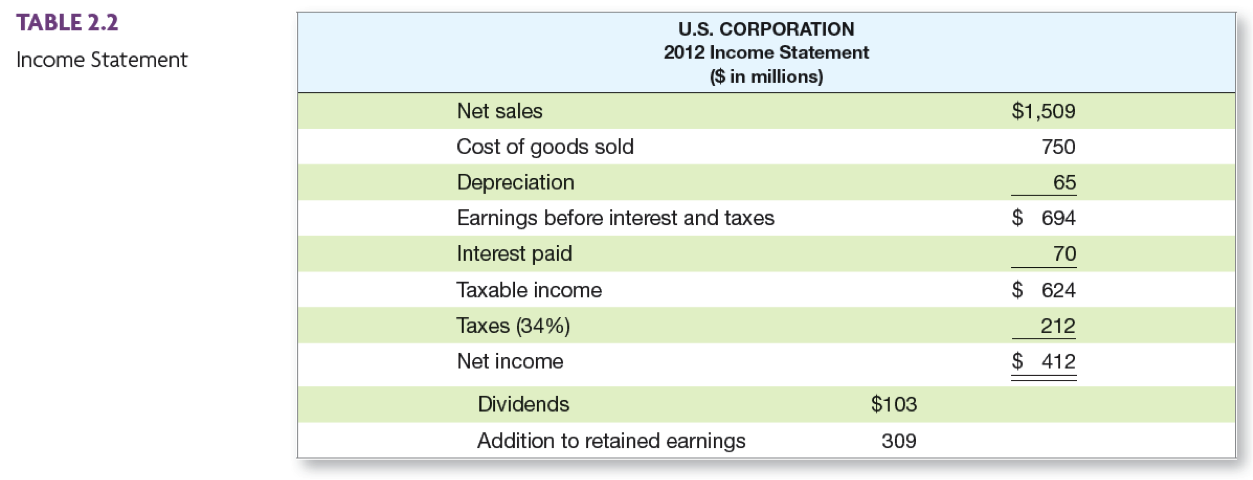

Income Statement

- See Table 2.2

- Cash flows over time: Revenues - Expenses = Income

- Evaluating a income statement

- GAAP

- Revenue - recognition (time of sale not collection)

- Expenses - matched with revenue

- Subject to managerial discretion?

- Non-cash items (depreciation)

- Time and costs

- Finance: fixed and variable costs

- Accounting: product and period costs

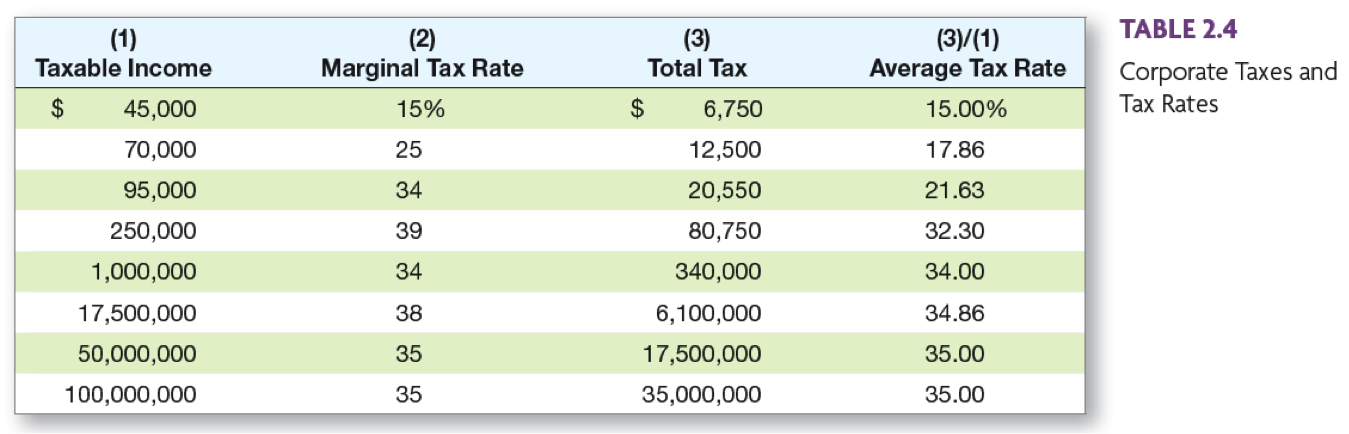

Taxes

- Marginal vs. average tax rates

- See Table 2.3 for tax schedule and Table 2.4 for example calculations

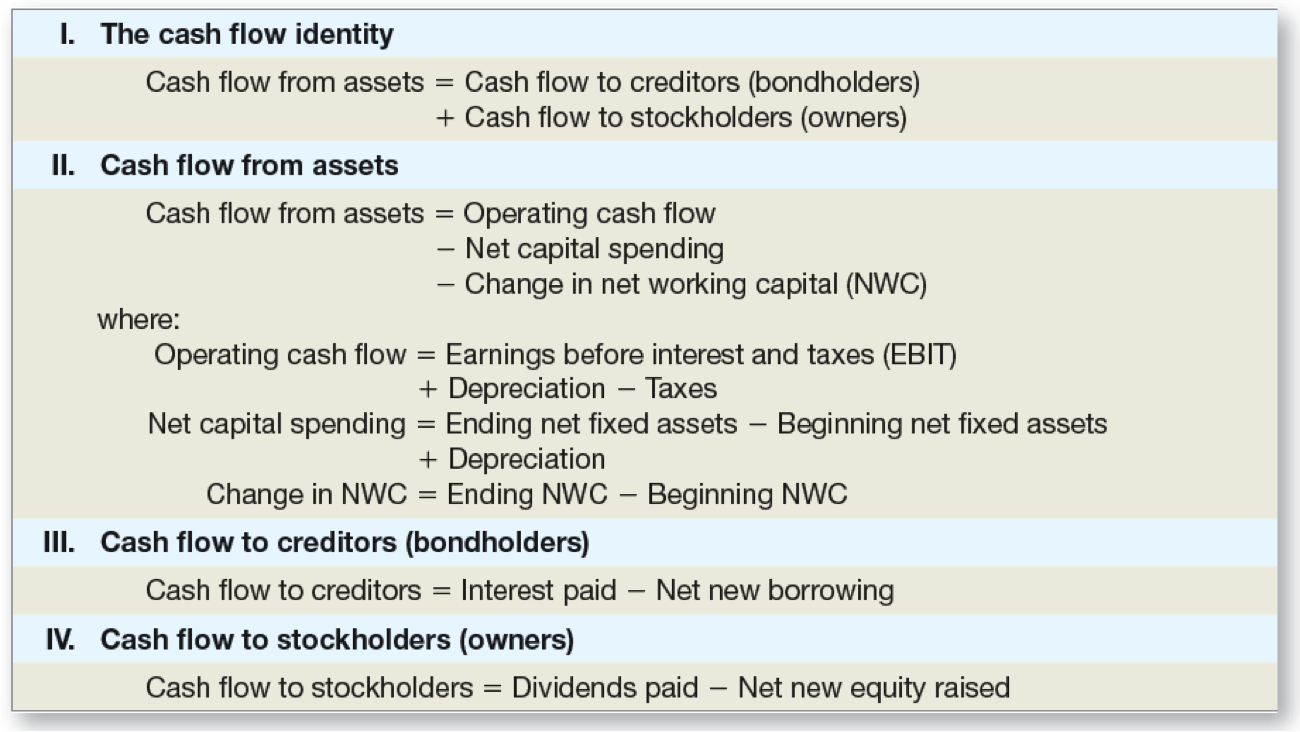

Cash Flow

- See Table 2.6 for formulas

- Cash flow from assets

- Subject to our accounting identity

- Consists of three parts:

- Operating cash flow

- day-to-day activities of producing and selling (no non-cash outflows or financing expenses)

- Do inflows cover outflows?

- Capital spending (CapEx): change in fixed assets not including depreciation

- Change in net working capital (short-term assets less short-term liabilities)

- Cash flow to creditors: Interest paid - Net new borrowing

- Cash flow to stockholders: Dividends paid - Net new equity raised

{kind=link}

{kind=link}

{kind=link}

{kind=link}