Processing math: 100%

Ch. 16: Financial Leverage and Capital Structure Policy

Capital Structure

- Capital Structure is the amount of debt and equity a firm uses as its sources of capital.

- How should a manager decide between debt and equity financing?

- What should the manager’s goal be?

- Maximize shareholder value.

- When does this differ from maximizing firm value?

- How does maximizing firm value relate to WACC?

- Management should choose capital structure to maximize shareholder wealth. This can be achieved by maximizing firm value or minimizing WACC.

- How can management alter capital structure?

- Increase leverage

- Increase debt

- Reduce equity by repurchasing shares (paying a dividend)

- Decrease leverage

- Retire outstanding debt

- Issue new equity

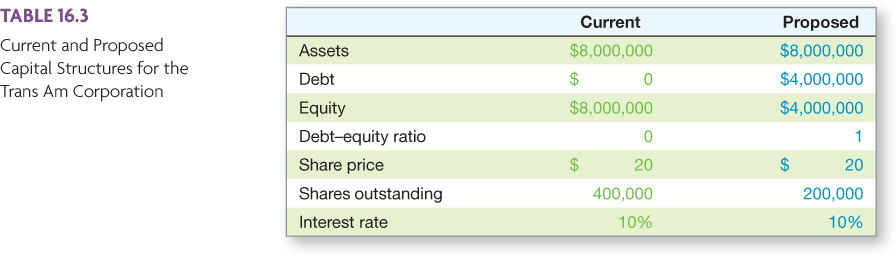

Effect of Leverage

Break-even EBIT

- We are trying to find the Earnings Before Interest and Taxes (EBIT) where the Earnings Per Share (EPS) is the same under both the current and proposed capital structures.

- See Figure 16.1.

- If we expect the EBIT to be greater than the break-even point, then leverage may be beneficial to our stockholders.

- If we expect the EBIT to be less than the break-even point, then leverage is detrimental to our stockholders.

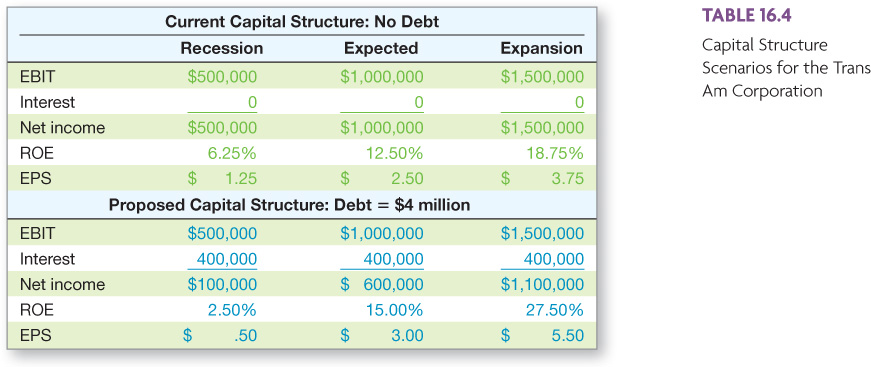

- Conclusions

- The effect of financial leverage depends on the company’s EBIT. When EBIT is relatively high, leverage is beneficial.

- Under the expected scenario, leverage increases the returns to shareholders, as measured by both ROE and EPS.

- Shareholders are exposed to more risk under the proposed capital structure because the EPS and ROE are much more sensitive to changes in EBIT in this case.

- Because of the impact that financial leverage has on both the expected return to stockholders and the riskiness of the stock, capital structure is an important consideration.

Homemade Leverage

- Why is this last conclusion not the case?

- As an investor, I can use personal borrowing to undo the capital structure decisions of the manager.

- If the proposed capital structure from the previous example is not implemented, how can I get equivalent exposure to the levered case?

- I am interested in owning 100 shares in the levered firm.

- I can achieve this payoff by buying 100 shares outright and buying 100 shares by borrowing at 10%.

Modigliani-Miller Theorem

- Three cases

- No corporate taxes, no personal taxes, no bankruptcy costs

- Corporate taxes, no personal taxes, no bankruptcy costs

- Corporate taxes, no personal taxes, Bankruptcy costs

- Two Propositions

- Firm Value

- Can change due to the riskiness of cash flows

- Can change due to changing the cash flows (amounts and timing)

- WACC and Systematic Risk

Capital Structure Theory without Taxes

- Modigliani-Miller Proposition I

- The value of the firm is not affected by changes in the capital structure.

- The cash flows of the firm do not change; therefore, value doesn’t change.

- Modigliani-Miller Proposition II

- WACC is not influenced by capital structure.

- WACC=RA=EVRE+DVRD

- RE=RA+DE(RA−RD)

- See Figure 16.3.

- Examples

- Required return on assets = 16%; Cost of debt = 10%; Percent of debt = 45%. What is the cost of equity?

- Required return on assets = 16%; Cost of debt = 10%; Cost of equity = 25%. What is the Debt-to-Equity ratio?

- How does financial leverage change systematic risk?

- Plug CAPM into above equation.

- βE=βU+DE(βU−βD)

- If debt is riskless, βE=βU(1+DE).

Capital Structure Theory with Taxes

- Modigliani-Miller Proposition I

- When a firm adds debt, it reduces taxes.

- The reduction in taxes increase the firm’s cash flows.

- The value of the firm increases by the present value of the annual interest tax shield ((Tc×D×RD)/RD=Tc×D).

- VL=EBIT(1−Tc)RU+DTc

- Example: EBIT = $25 million; Tax rate = 35%; Debt = $75 million; Cost of debt = 9%; Unlevered cost of capital = 12%.

- See Figure 16.4.

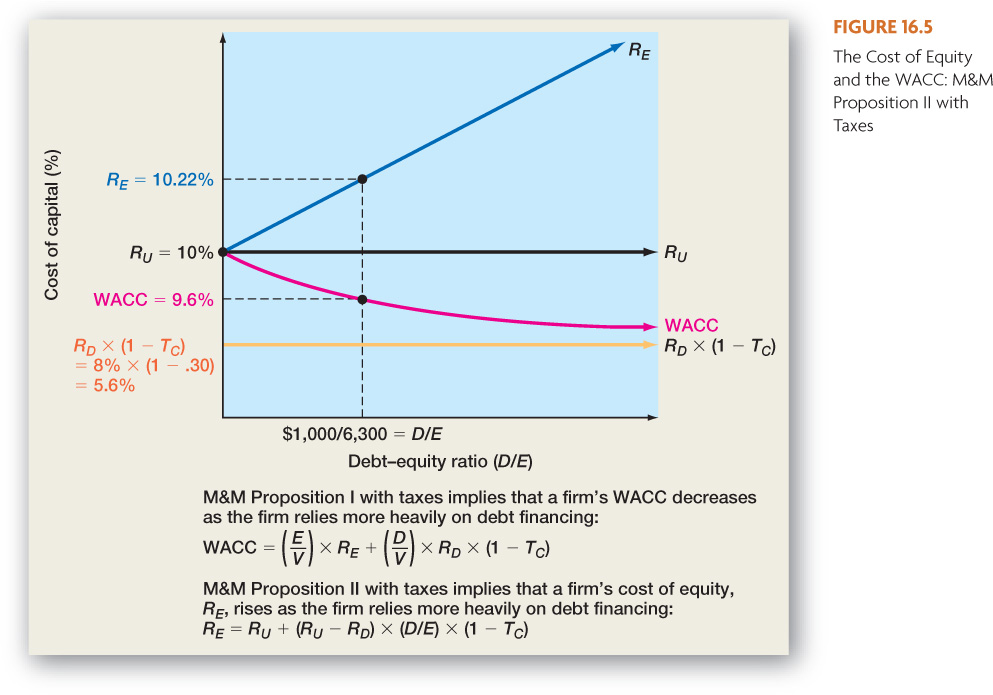

- Modigliani-Miller Proposition II

- WACC decrease with leverage because the government subsidizes interest expenses.

- WACC=RA=EVRE+DV(1−Tc)RD

- RE=RU+DE(1−Tc)(RU−RD)

- See Figure 16.5.

- How does financial leverage change systematic risk?

- Plug CAPM into above equation.

- βE=βU+(1−Tc)DE(βU−βD)

Trade-off Theory of Capital Structure

- As leverage increases, the probability of bankruptcy increases.

- The increase probability of bankruptcy increases the expected bankruptcy costs.

- Bankruptcy Costs

- Direct

- Legal and administrative costs

- Liquidity costs of selling

- Indirect

- Assets lose value as management spends time worrying about avoiding bankruptcy instead of running the business.

- The firm may also lose sales, experience interrupted operations and lose valuable employees.

- The value of the firm is maximized when the costs of bankruptcy exactly offset the present value of the interest tax shield.

- See Figure 16.6.

- See Figure 16.7.

Managerial Recommendations

- The tax benefit is only important if the firm has a large tax liability.

- The risks of financial distress:

- The greater the risk of financial distress, the less debt will be optimal for the firm.

- The cost of financial distress varies across firms and industries, and as a manager you need to understand the cost for your industry.

Pecking-Order Theory

- According to Pecking-Order Theory:

- Use internal financing first.

- Issue debt next.

- Issue new equity as a last resort.

- This theory is at odds with tradeoff-theory:

- There is no target D/E ratio.

- Profitable firms use less debt.

- Companies like financial slack (cash on hand).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}