Ch. 15: Raising Capital

Early-Stage Financing and Venture Capital

- Private financing for new businesses in exchange for equity.

- May be individuals (angels)

- May be pooled (private equity) funds

- Usually entails some hands-on guidance.

- Funding usually comes in stages.

- ``Seed money’’ or ground floor financing

- Mezzanine financing

- VC companies usually have an exit strategy.

- Sell the company

- Take the company public

Types of Public Equity Issues

- General cash offer: an issue of securities offered for sale to the general public

- Initial public offering: a company’s first equity issue made available to the public

- Seasoned equity offering: a company’s subsequent equity issues

- Rights Offering

- A public issue of securities in which securities are first offered to existing shareholders

- Helps with dilution problem

- Uncommon in US

Underwriters

- An investment firm that serves as an intermediary between the issuing company and investors

- Underwriters perform the following services:

- Formulate the method used to issue the securities.

- Price the new securities.

- Sell the new securities.

- Provide price stabilization.

- Typically, the underwriter will buy the shares at less than the offer price. This gross spread serves as the underwriter’s compensation.

- A group of underwriters is called a syndicate.

- Types of underwriting

- Firm Commitment: the underwriter buys the entire issue

- Best Efforts: underwriter can return unsold shares

- Dutch Auction

- offer price is set based on competitive bidding by investors

- price paid is the highest price that will result in all shares being sold

- Additional Terms

- Green shoe provision: allows for oversubscription (underwriter can purchase an additional 15% of the issue)

- Lockup agreement: specifies how long insiders must wait after an IPO before they can sell their shares

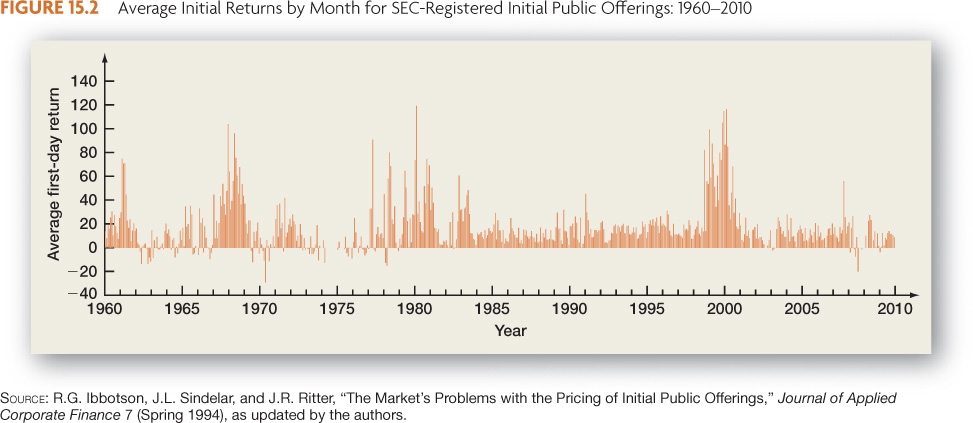

IPO Underpricing

- See Figure 15.2.

- Money left on the table

- Potential explanations for underpricing:

- Much of the apparent underpricing is attributable to smaller, more speculative issues.

- Winner’s curse: Suppose there are two investors, Joe Average and Ms. Smarts. Ms. Smarts avoids overpriced issues and heavily invests in underpriced issues. Joe Average puts in a bid for all IPOs. As a result, he gets more of the duds and fewer of the underpriced shares. To keep Joe bidding, firms underprice new shares.

- Legal liability

Seasoned Equity Offerings

- Stock prices tend to decline following the announcement of a new equity issue.

- Why?

- Managerial information: issuing equity is cheapest when the firm is overvalued

- Debt usage: If the new projects are good, why make them available to new shareholders?

- Issue costs: Indirect costs of selling securities (e.g., management time)

Dilution

- Dilution is a loss in value for existing shareholders.

- Percentage ownership: shares sold to the general public without a rights offering

- Market value: firm uses new capital on negative NPV projects

- Book value and EPS: occurs when market-to-book ratio is less than one

{kind=link}