Ch. 10: Making Capital Investment Decisions

Relevant Cash Flows

- We are interested in incremental cash flows.

- These are the cash flows that will only occur if the project is accepted

- We will treat each project in isolation from the current operations of the firm

- This is known as the stand-alone principle.

- Think of the project in question as a mini-firm.

- Focus on:

- cash flows

- timing (when you get the money, not when it accrues)

- cash flows net of taxes (taxes are a cash outflow)

- Ask the question: “Will this cash flow occur only if we accept the project?”

- If you answer “yes,” then include the cash flow.

- If you answer “no,” then don’t include the cash flow.

- If you answer “partly,” then include the part that occurs because of the project.

- Common Pitfalls

- Sunk Costs

- a cost that has already been incurred

- not an incremental cash flow

- Opportunity Costs

- most valuable alternative (cost of lost options)

- include as an incremental cash flow

- Side Effects (spillovers)

- Positive

- Negative: “erosion” (cash flows of existing projects are reduced)

- include as an incremental cash flow

- Net Working Capital

- inventories

- accounts receivable (sales on credit)

- accounts payable (supplies on credit)

- include as an incremental cash flow

- Financing Costs

- not an incremental cash flow

- analyze separately

- included in required rate of return (cost of capital)

- Taxes

- represent a cash outflow

- include as an incremental cash flow

Pro Forma Statements

- Financial statements projecting future years’ operations

- How do we get from accounting statements to cash flows?

- Operating Cash Flow (OCF) = EBIT + Depreciation - Taxes = Net Income + Depreciation

- Cash Flow from Assets (CFFA) = OCF - Net Capital Spending - Changes in NWC

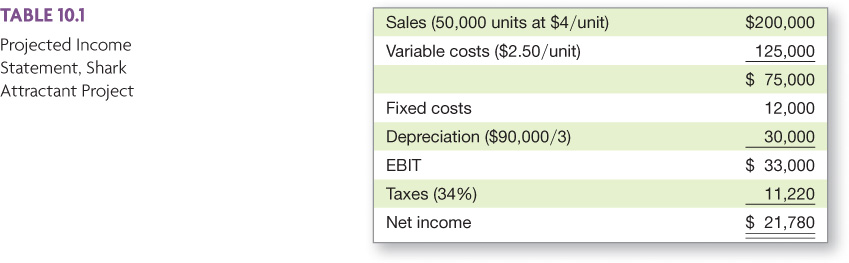

- Example - Shark Repellant

- See Table 10.1

- See Table 10.2

- OCF = $51,780, Capital Spending in Year 0 = $90,000, NWC Outflow in Year 0 = $20,000, Return of NWC in Year 3 = $20,000

- NPV = $10,648 at required rate of return of 20 percent; Payback Period = 2.1 years

Details

- Net Working Capital

- GAAP requires that sales be recorded on the income statement when made, not when the cash is received.

- GAAP also requires that we record the cost of goods sold when the corresponding sales are made, whether we have actually paid our suppliers to date.

- Finally, we have to buy inventory to support sales, although we haven’t collected cash yet.

- Depreciation

- Depreciation itself is a non-cash expense; consequently, it is only relevant because it affects taxes.

- Straight-line: D = (Initial cost – salvage) / number of years

- MACRS: See Tables 10.6 and 10.7

- After-tax Salvage

- If the salvage value is different from the book value of the asset, then there is a tax effect.

- Book value = initial cost – accumulated depreciation

- After-tax salvage = salvage – T*(salvage – book value at time of sale)

- Taxes can be positive or negative

- Example: Purchase price = $110,000, Salvage Value in Year 6 = $17,000, MTR = 40 percent

- Straight-line: After-tax salvage = $17,000

- 3-year MACRS: After-tax salvage = $10,200

- 7-year MACRS: BV in Year 6 = $14,729, After-tax salvage = $16,091.60

Alternative Definitions of OCF

- Bottom-up: OCF = NI + Depreciation (only valid if no interest expense)

- Top-down: OCF = Sales - Costs - Taxes

- Tax Shield

- OCF = (1-T)(Sales - Costs) + T*Depreciation

- Depreciation Tax Shield

Examples

- Cost Cutting

- $80,000 in equipment. Save $22,000 per year (before taxes). Straight-line depreciation to zero in 5 years. Salvage of $20,000. Tax rate is 34 percent, and the discount rate is 10 percent.

- After-tax Salvage = $13,200, OCF = $19,960, NPV = $3,860

- Setting the Bid Price

- A local distributor has requested bids for 5 specially modified trucks each year for the next four years. Each truck costs $14,000 in materials plus facilities must be leased for $24,000 per year. We need $60,000 of new equipment. Depreciate to zero over four years (straight-line). Salvage value is $5,000. We need $40,000 in working capital. Tax rate is 39 percent. What price should we bid for a 20 percent return?

- OCF = $30,609, NI = $15,609, Sales = $134,589 or $26,918 per truck

- Evaluating Equipment Options with Different Lives

- Machine A costs $100 to buy and $10 per year to operate. It wears out and must be replaced every two years. Machine B costs $140 to buy and $8 per year to operate. It lasts for three years and much then be replaced. Ignoring taxes, which one should we choose if we use a 10 percent discount rate?

- Machine A: NPV = $–117.36; Machine B: NPV = $–159.89

- Equivalent Annual Cost: annuitize cost to annual basis

- Machine A: EAC = $–67.62; Machine B: EAC = $–64.29

{kind=link}

{kind=link}